Gold is not everything, but everything needs gold.

– Russian Proverb

Over a year ago, I wrote an article. Is it possible that Trump actually has an economic policy?

It was the eve of Pope Francis’s funeral, and my thoughts were drifting toward the possible changes a new papacy might bring — perhaps even a decisive shift in the Catholic direction of travel. The prospect of an American Pope arriving alongside a wannabe Pentecostal-born-again Son-of-the-Prairie President seemed, at the very least, geopolitically intriguing.

That, in turn, led me to wonder whether Donald Trump’s apparently chaotic economic behaviour might conceal something more strategic. Being a gent, I erred on the side of generosity.

In that earlier piece, I suggested — perhaps somewhat clumsily — that the world was beginning to move away from the post-Cold War globalised financial order and toward something far more fragmented: a strategic, reserve-competition era.

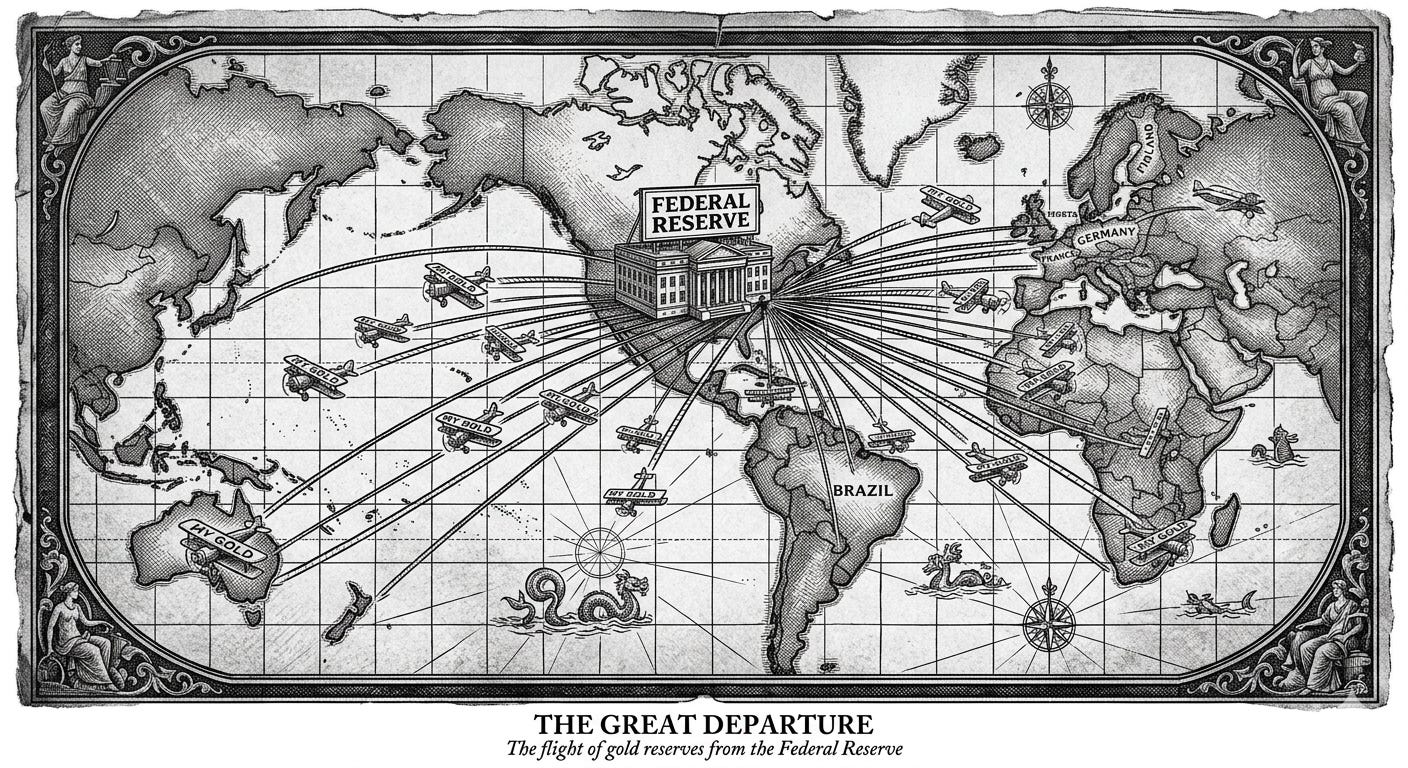

And the signs are everywhere - as has been widely reported over the past eighteen months, an increasing number of nations have begun quietly bringing strategic reserves home.

France has now completed the repatriation of its gold from New York. Germany continues to debate doing the same. Poland has aggressively expanded its bullion holdings. Serbia has announced that all of its gold will now be held domestically. Across the BRICS nations, reserve diversification away from dollar-denominated assets has accelerated noticeably.

Each of these developments can be dismissed individually as technical, administrative, or politically symbolic. Taken together, however, they suggest something much larger: trust itself is beginning to fragment.

For decades, the post-Bretton Woods order rested upon a series of assumptions which most of us scarcely noticed because they appeared permanent. The United States dollar was regarded not merely as the dominant reserve currency but as politically neutral. American financial institutions were assumed to exist outside the turbulence of ordinary geopolitics. Western custody of sovereign assets was considered unquestionably safe. And now somewhere I suspect, there’s a Head of Risk in some global financial empire who is saying, “You have got to be kidding me.”

The freezing of Russian reserves after the invasion of Ukraine may ultimately come to be seen as one of the great financial turning points of the modern era. Whatever one’s view of Russia — and mine is far from sympathetic — the precedent itself mattered enormously. In one stroke, every central bank on Earth was reminded that reserves held abroad are only sovereign for so long as the custodian power remains politically aligned with you.

That changes the psychology of reserve management entirely. Couple that with a U.S. president who globally and very publicly diminishes at least four heads of state within three months, and “taking a view” on your relationship might make you pause.

Gold stored in Manhattan suddenly ceases to look like prudent international cooperation and starts looking like strategic dependence. Treasury holdings begin to carry geopolitical as well as financial risk. Access to payment systems, clearing systems, and reserve liquidity can no longer be assumed to exist beyond politics. The era in which economics and geopolitics occupied separate rooms appears to be ending.

And so gold returns.

Not because nations expect to return to the Gold Standard, nor because central bankers have suddenly become romantics, but because physical bullion possesses one quality increasingly prized in an unstable world: neutrality.

Gold cannot be sanctioned electronically. It cannot be printed by a foreign parliament. It cannot be frozen with the stroke of a Treasury pen if it sits beneath your own capital city. In an age of strategic uncertainty, sovereignty itself is once again becoming an economic asset.

This, I think, is the deeper story unfolding beneath the daily noise of tariffs, trade disputes, sanctions, and currency arguments. We are witnessing the slow emergence of what I earlier described as a reserve-competition era — a world in which nations increasingly compete not merely for military or industrial strength, but for monetary resilience, reserve independence, and strategic insulation from one another.

Ironically, America itself may have accelerated this transition.

By weaponising tariffs, sanctions, access to reserves, export controls, and the dollar system itself to pursue geopolitical objectives, Washington demonstrated the extraordinary power of the post-Cold War financial order. Yet in doing so, it also encouraged the rest of the world to begin quietly constructing escape routes from it.

Empires often weaken not when their power disappears, but when their power begins to look unpredictable.

Gold and its malleability also triggered a distant memory of a conversation some eight years ago about a company called Glint. It launched with enormous ambition around 2017–18 as a gold-backed payments platform. Users could buy allocated gold stored in Swiss vaults and spend against it with a Mastercard. Sadly, in 2019, it fell into administration after a hostile takeover and debt dispute involving a Singapore investment consortium called Nimoi Holdings. Customer funds were temporarily frozen and then released after Glint emerged from administration, having raised emergency funding and continued operating. It still exists, though more as a niche asset-backed fintech than a transformational monetary platform.

The tragedy - because I thought it was a brilliant idea - was not the concept, which was simply too early, all the other issues, such as regulatory complexity, payments infrastructure costs, scaling difficulties, consumer inertia…. and the fact that most people still think in fiat currency terms.

Glint was trying to solve a philosophical problem before most people even believed it existed. The investment and promotional arguments Glint made over seven years ago now sound much less eccentric. Everything I have suggested above is now supporting their core proposition: “Gold should function as spendable money again.” At the time, that sounded fringe. But in a world increasingly concerned with reserve sovereignty and distrust of purely digital fiat systems, the underlying logic no longer seems entirely outlandish. I, for one, would be unsurprised to see a Glint in the distance.